The automotive industry is proving resilient

Interruptions in the supply chain, demand fluctuations and the shutdown of production during the first lockdown in the spring of 2020 severely tested the automotive industry last year. As a result, car production fell by 16% between 2019 and 2020.

However, the pandemic has also impacted the working capital management (WCM) of OEMs and suppliers: For instance, for a time the capital commitment period in the second quarter of 2020 rose to 60 days, but settled back down a 33 days at the end of the year – and is thus four days higher than in 2016. In particular, the manufacturers’ working capital performance has deteriorated here, while suppliers were able to improve their WCM.

These are the results of a PwC analysis of more than 800 companies from the automotive industry.

“During the crisis, the automotive industry displayed enormous resilience. Following the stoppage in the spring of 2020, it has recovered relatively quickly. Nevertheless, as yet it has been unable to regain its strength from the period before the pandemic.”

Study overview

The capital commitment period has increased among OEMs

The capital commitment period of the original equipment manufacturers (OEMs) has increased by 10 days in the last five years and stood at an average of 27 days at the end of 2020.

Crisis-struck 2020 accounts for a large portion of this deterioration: Due to industry-wide plant closures and supply chain difficulties, the capital commitment period even rose to 53 days in the second quarter of 2020.

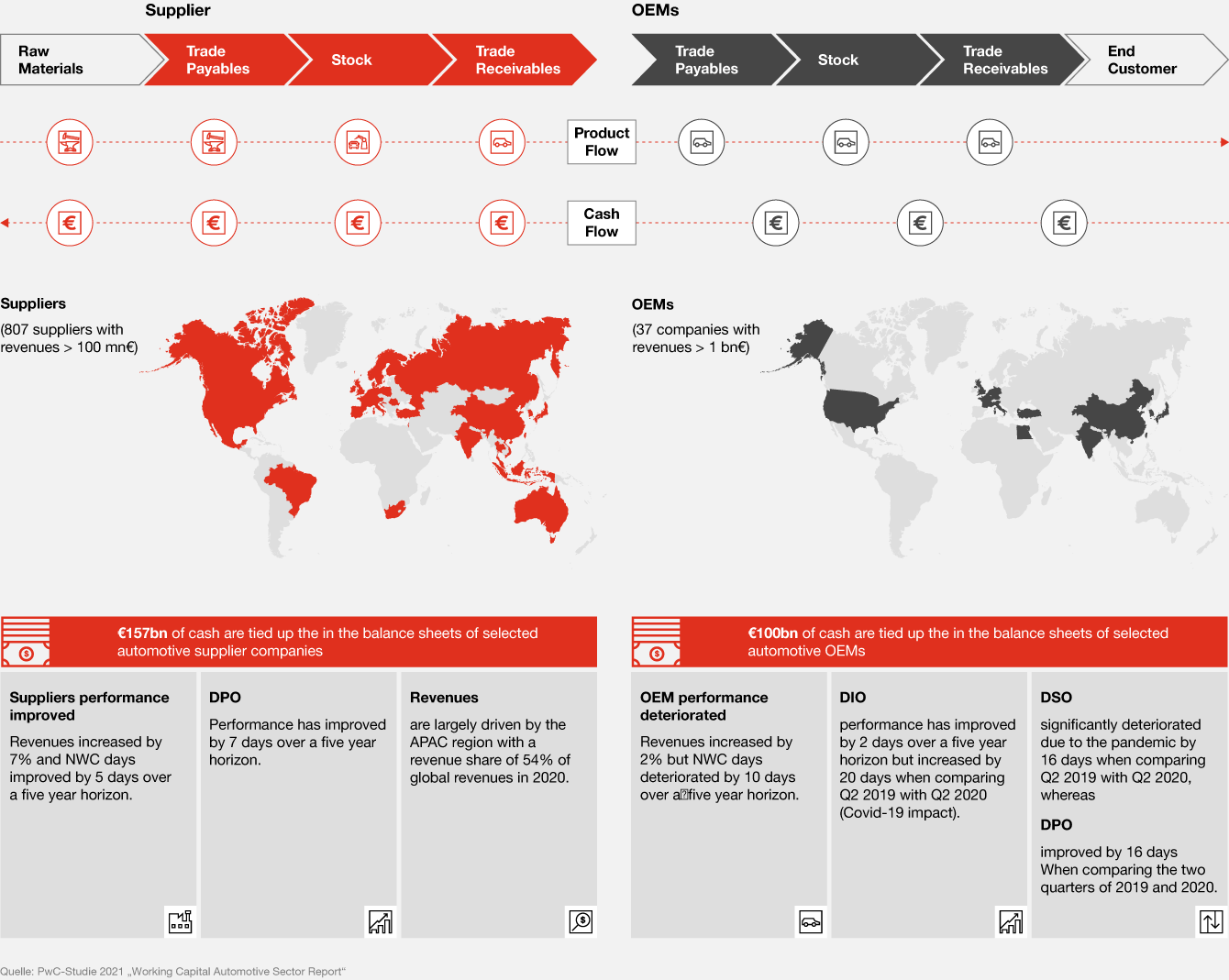

However, in the second half of the year the industry was slowly able to recover and further improve its performance in the area of working capital management. Nevertheless, at the end of 2020 the 57 OEMs analysed had committed capital of around € 100 billion – money that is missing elsewhere, for instance for innovations.

Five-year comparison of DIO, DSO and DPO among OEMs

The inventory range (days inventory on-hand, DIO) among OEMs – in other words, the period between receipt and withdrawal of goods – fell by one day in the last five years (2016 to 2020) and stands at 37 days.

The days sales outstanding (DSO), in other words, the period of time between the order date and receipt of payment, has noticeably deteriorated and has risen to 36 days (an increase of 8 days). This development is primarily attributable to the pandemic and customers’ weaker capacity to pay.

The days payables outstanding (DPO), in other words, the period between the invoice date and payment, has fallen by 4 days in the last five years – and now stands at 45 days.

Suppliers can improve their WCM

Unlike the manufacturers, suppliers have managed to improve their cash management in the last five years. The capital commitment period for the automotive suppliers analysed fell by five days during this period and stood at 44 days at the end of 2020 (2016: 49 days).

It is true that the coronavirus pandemic has had an impact on suppliers' working capital performance. The capital commitment period temporarily stood at 73 days in the second quarter of 2020. However, companies were able to reverse these effects and concluded 2020 with a positive WCM balance.

DPO, DIP and DSO among suppliers

In the last five years, the range of days payable outstanding (DPO) rose by seven days and stood at 62 days at the end of 2020.

The days inventory on-hand (DIO) increased by one day during a five-year period and stood at 42 days at the end of 2020. In the second quarter of 2020 it had temporarily risen to 67 days.

The days sales outstanding (DSO) rose by two days with suppliers since 2016 and now stands at 64 days. In the second quarter of 2020 this indicator temporarily rose to 82 days.

COVID impacted on the entire value stream of Supplier and OEMs

Tips to optimise cash management

- Identify and realise cash and cost advantages along the entire value chain.

- Optimise the operational processes that support the working capital cycle.

- Increase transparency and performance through data analyses and digital solutions.

- Make sure that you have rapid cash conversion in times of crisis.

- Develop resistant supply chains in order to be prepared for unexpected risks and interruptions.

- Build up a “cash culture” and provide ongoing training to your organisation to this end.

- Apply digital solutions for retail and supply chain.

Five steps towards greater resilience

- Cash governance

- Sensitizing employees

- Data and transparency

- Processes

- Supply chain

Cash governance

Do our guidelines, goals and incentives contribute to helping us to reach the correct decisions?

Companies must adapt their governance frameworks in such a way as to ensure that they address possible conflicts of goals and that the organisation has suitable guardrails for its operational business.

Sensitizing employees

Do our employees have the required framework and skills to reach the correct decisions?

The operational functions must support employees in helping them to reach the correct decisions and prevent a “business as usual” approach.

Data and transparency

Is the right operational data available to support rapid decision-making?

Historical models on which most processes are based are only useful to a limited extent. Transparency is required in real time in order to reach informed decisions.

Processes

Do our cash processes still fit the new normality?

The operational processes in the area of working capital management must be adapted to the new normality. For instance, in the area of receivables it is about renegotiating the payment terms; for inventory management, demand forecast models must be tested, and for liabilities, companies should tackle the opportunities offered by supply chain finance, among other things.

Supply chain

How resilient is my supply chain?

Companies must obtain clarity around their financial situation and their suppliers’ delivery capacity and develop an emergency plan.

“The COVID-19 pandemic has emphasised the importance of working capital management. In the current situation it is more important than ever to minimise the proportion of committed capital, secure liquidity and increase flexibility.”

Cash to drive the shift: Working Capital Automotive Sector Report

Any questions?

The methodology

These are the results of a PwC analysis of more than 840 companies from the automotive industry worldwide, including 37 OEMs and 807 suppliers.

Related content

Follow us

Contact us