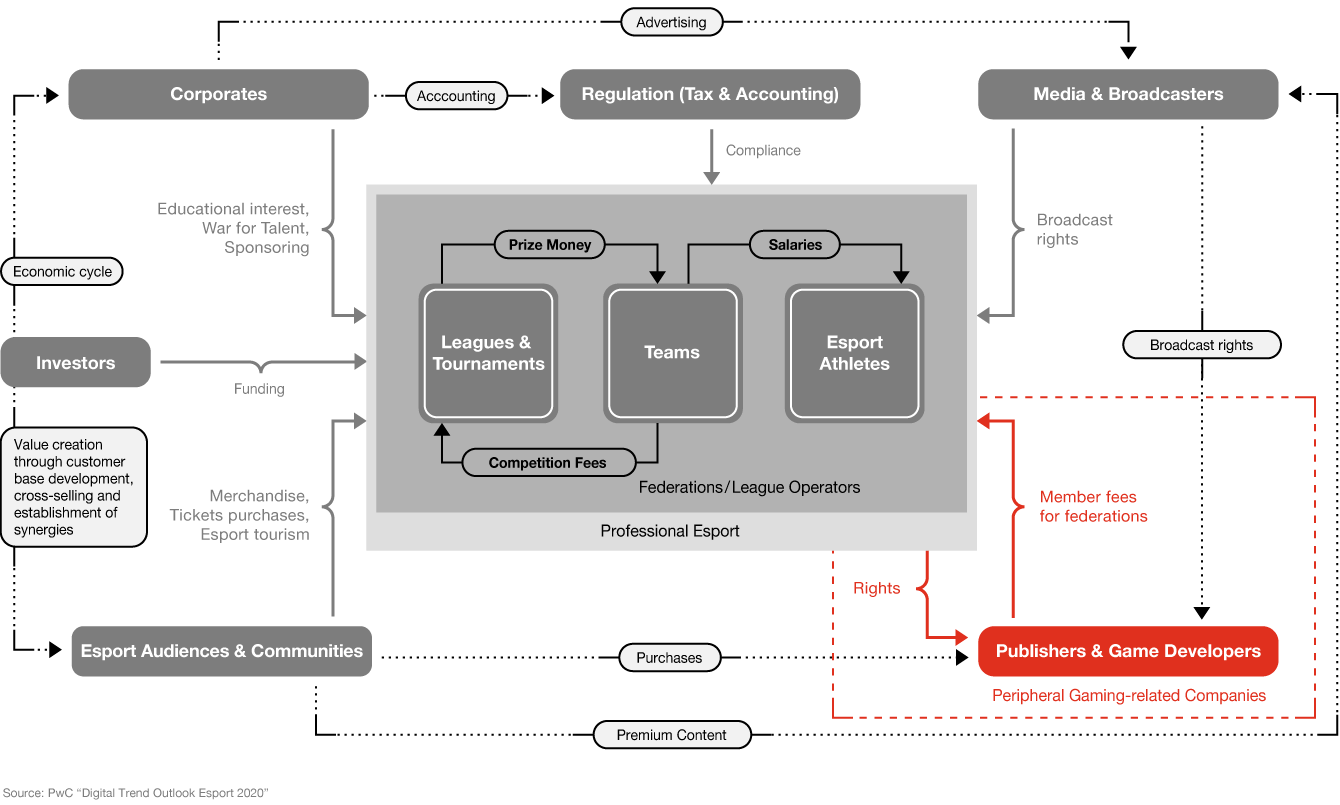

Publishers & Game Developers: The mighty ones within

By Gian Luca Vitale. Esports would not exist without publishers and game developers. Those same companies also host and produce coverage for some of the scene’s largest competitions, such as Riot Games’ League of Legends Worlds, Valve’s Dota 2 The International or the Counter-Strike: Global Offensive Intel Extreme Masters. Publishers that own the intellectual property rights are the most powerful and most relevant players in the esports ecosystem. They can either advance or cut down the development path of an esports title and are therefore leading the development of an entire sub-ecosystem that could be built around an esports title. When it comes to competitions or events, publishers license their esports titles to endemic and non-endemic players or third parties such as league operators (ESL, Dreamhack, Starladder, etc.), streaming platforms (Twitch, YouTube, Huya, etc.), esports teams (Cloud9, Team SoloMid, G2 Esports, etc.) or brands (Red Bull, MasterCard, Mercedes-Benz, etc.). In this way, they share their business risk and generate revenue through license fees while broadening their intellectual property and fostering business relationships.

Now more than ever, there is an increasing incentive for publishers to turn their new competitive titles into esports games, with the benefits including extraordinary exposure, both online and offline, and revenue that can be generated from competition-themed in-game content as a free2play game, for example. Currently, esports is in a phase of change and appears to be evolving from being a player acquisition and retention tool for publishers to being its own industry, with far greater speed and stronger professionalism. Network effects, the formation of economic ecosystems and the creation of sustainable communities are the central aspects of future development. It is clear that publishers are a leading force when it comes to the development of economic ecosystems. Here too, we will see which publishers seize the “peeker’s advantage” and build up their networks faster, promote adaptation rates and proactively ensure professional structures in order to gain a decisive competitive advantage.

Publishers striving for dominance and those carving out their niches

The publishers Riot Games, Valve, Activision Blizzard, Epic Games and Electronic Arts are the largest competitors in the esports industry with their game titles that have been established for many years now. What unites all of them is the desire to enthuse masses of players for their different esports titles. But what makes them different is how they develop their esports ecosystems and the esports titles as entertainment software products. The development and successes surrounding the growth of esports consistently follow the laws of economic ecosystems, network effects and economies of scale which are catalyzed in particular by human social factors and the synergy between a seamless and comprehensive digital and physical experience. As a result, publishers are more concerned than ever with consolidating their economic ecosystems with other endemic players, such as esports teams and league operators, and with non-endemic drivers, such as early-stage investors and sponsors. The competition for the attention and favor of gamers and the community is intensifying and will become even more intense in the future.

The types of adaptation and the goal of winning and inspiring as many gamers as possible for the esports titles are of the essence. Above all, publishers are trying to keep the entry barriers to the respective esports titles as low as possible in order to make it easier to test them and to monetize the esteem of gamers in the long term through in-game transactions. Because this will clearly continue to be decisive for the success and life cycle of esports titles in the future, the larger the player base, the more attention an esports ecosystem receives from brands, teams, sponsors and investors, which in turn can increase the added value of the players as a whole. Even those ecosystems with a correspondingly high number of players have more potential in the long term due to government subsidies. Mastering direct and indirect network effects becomes more important than ever before.

This growth is favored not only by developments within games and the professional esports structures in and around games, but also by the investments around community building and the possibilities for gamers, content creators, influencers and streamers to share experiences and to offer an esports title a home for a community. As a result, the human social aspect is becoming a key success factor in the development of economical esports ecosystems and will play an even stronger role in determining which publishers will win the race to establish economically sustainable esports ecosystems.

In essence, every esports title is a social network in its own right and must be understood as such in the future, with more or less pronounced structures and experiences that bind the players together. With regard to the use of lock-in effects for an ecosystem, the human social aspect takes on even greater significance. Free2play models are currently making a major contribution to ensuring that everyone can try out games without any major financial risk. At the same time, the switching costs for users are correspondingly low, meaning that gamers will migrate more quickly if the game experience is disappointing. However, the peer group, the community, acquaintances and friends are known to be important factors in deciding which games are preferred. In addition, as soon as the first investments in in-game assets are made, the lock-in effect starts to increase and the likelihood of switching slowly begins to decrease. If publishers manage to keep a large part of the community for themselves, the level of enjoyment within the group is supposedly greater. This peer dynamic can also help to convince more and more players of esports titles, even if these players did not like the games at first. From an economic point of view, social mechanisms will continue to influence the positive adaptation rate in the future, contributing to long-term success in competition between publishers and game developers.

At the same time, enthusiastic players take on the role of attracting players who may not often try out new games or shy away from trying games due to unfounded prejudices. This effect at the casual gamer level spreads throughout the entire ecosystem up to esports organizations and professional competition. Particularly promising for the brand identity and effectiveness of esports organizations are esports titles with a wide range of players, fans and enthusiasts. Esports teams and successful esports titles with such a base therefore invest more into their networks in order to capitalize on this, helping attract sponsors, build up teams and channels and create more competition products and events. Such parties are very interested in avoiding a reduction and a change in their networks, even though esports organizations are known to react especially flexibly and dynamically to market changes. Sponsors and brands are particularly concerned about stability and predictability in a commitment, which makes the importance of sustainable development and use of network effects all the more crucial to success and will make them all the more powerful in the future.

This development has already progressed to varying degrees for the various esports titles, which are essentially products for sports, entertainment, socialization and leisure activities. As a result, publishers are pursuing different objectives in terms of market penetration, market development, diversification and product development based on the degree of maturity and the distribution or user numbers of the esports titles. Those looking to be part of this industry and planning to enter the market need to closely monitor the strategy and activities of publishers and evaluate them according to the factors mentioned above. Only if these factors are taken into account when developing a market entry or go-to-market strategy can they successfully benefit from the increasing development of the respective esports ecosystems. As in any case, the race to adapt, win the favor of the community and build the strongest economic ecosystems is in full swing, with sponsors, partners, investors, athletes and fans, both endemic and non-endemic.

Racing games—out of their niche and into uncertain times

Driven primarily by popular racing drivers streaming and participating in virtual events, sim racing experienced a large boost in attention after motorsports ground to an abrupt halt due to COVID-19. A list of the most well-known motorsports series has now started sim racing initiatives. Formula One has organized a series of F1 Virtual Grand Prix events in lieu of its real races in cooperation with the esports organizer Gfinity using the official F1 2019 game developed by Codemasters. Motorsport Games’ biggest single event project was the 24 Hours of Le Mans Virtual, which took place on June 13 and 14 in lieu of the actual race, having been postponed until September. A cumulative audience of over 14.2 million tuned into the show in 57 different countries worldwide on mainstream channels such as Eurosport, ESPN, Sky Sports and J-Sports to follow the virtual race. On digital channels, the 24 Hours of Le Mans Virtual gathered over 8.6 million views across Facebook, YouTube and Twitch. The pandemic has moved sim racing esports forward several years, with people now more capable of appreciating what sim racing and esports can mean to a real motorsports series. This creates an ever closer connection between real motorsports and its esports version. Overall, an ecosystem is emerging that includes both variants equally, and fans often want to follow both of them. In the future, sim racing will be a part of racing itself, as a lot of academy programs are based on simulator driving, and may become a discipline in the world of motorsports too. In addition, more investors will be attracted to investing in sim racing esports, with the market in this esports segment continuing to expand even further. However, the elitist character and the opportunity to participate pose a danger for motorsports esports, especially sim racing. Due to the high cost of equipment for a professional and competitive sim racing setup, it is probably not possible for the masses to take their first steps in this area, which makes it less attractive compared to other segments. Here, motorsports esports has to avoid the problems of the past, otherwise sim racing will have a hard time sustainably expanding from its niche into the masses. The rest of the genre is still highly fragmented, with a large number of potential esports titles that still lack professional structures and publisher support. The next 1 to 2 years will be crucial in deciding in which direction the pendulum swings and whether motorsports esports has a bright future ahead of it. Now the main thing is to build a sustainable foundation and bring new ideas forward, rather than just copying the physical ecosystem. The focus should be on low entry barriers. They help to create a standard, develop a comprehensive league and competition system and, most importantly, unite the entire racing community to ensure further market penetration and market development.

Fighting games—the stalwart still searching for its way

Fighting games have one of the longest traditions in esports but have yet to achieve a lasting breakthrough in esports, despite having one of the most spectacular events: the Evolution Championship Series (EVO). Even the top publishers and game developers do not appear to be making any major efforts to create bigger esports ecosystems, although the passion of this community is unbelievable and would surely appreciate this. To make a real change happen, and to drive fighting games more out of its niche, they would need to establish comprehensive league structures on all competition levels and develop financial incentives and systems for players and esports organizations. This dilemma is particularly evident in the example of Nintendo. Despite an incredible installed base with the latest Nintendo Switch, eliminating the software-hardware paradigm problem, the potential has not been structured and exploited at full speed. Nintendo sees itself less as an active driver in building a top-down and bottom-up professional esports ecosystem, and more as a guiding partner in encouraging casual gamers in the community to become interested in competitive gaming following a strategy of organic and community-driven esports ecosystem development. Although this path could have led to success in the early days of the esport industry, the conditions for success are changing with the increasing competition of esports titles. Therefore publishers and game developers today need to take a more active and structured approach with all the ecosystem’s relevant players. The example reveals a systemic dilemma. The various esports titles are already competing for the attention of current and future esports athletes. Ecosystems without incentives, systems and structures have a hard time competing against the already existing offerings such as League of Legends, Counter-Strike: Global Offensive, Dota2, Rainbow Six Siege, Overwatch and Valorant. While the passion and love of the community is crucial, this love cannot be transformed and capitalized upon without the support and building of an ecosystem by publishers or third-party providers. It is already becoming apparent that we are experiencing a greater concentration in the market and that titles without a clear development outlook and investment will not make it to the top of the esports world in the future.

Riot Games—the thirst for more

During Riot Games’ League of Legends 10th anniversary celebratory stream, the company announced an unexpectedly large roster of new games and its expansion strategy for at least the next 3 to 5 years. For a company that has been built and focused on one title for a decade, this marks a major gear change in its ambitions and has caused an earthquake that provides a profound insight into what is to come in the years ahead. Riot Games is operating at an incredible speed, pursuing multiple strategies simultaneously with its existing and future products, from further market penetration and market development strategy with League of Legends and ever new league and competitive offerings in competitive, semi-professional and amateur classes, to the offensive attack with Valorant, an esports title to come with a related product development and diversification strategy. In doing so, Riot Games is pursuing its goal of bringing new impulses in various esports genres with its games. Riot Games could serve the entire esports ecosystem from a single source and thereby expand its economic ecosystem. Valorant plays a central part in this strategy and is a tactical, team-based FPS that was developed for esports. It combines the esthetics and some character-based play elements of Riots Games’ League of Legends with Valve’s Counter-Strike: Global Offensive. The choice of genre and target group is no coincidence, as the addressable market for tactical FPSs, and especially the success and popularity of Counter-Strike, has been known for decades. It therefore serves to foster the entry into a market where Valve has been able to operate almost without competition with Counter-Strike. At the same time, the brand image and brand awareness of Riot Games is to be used to transport Valorant faster into markets where Counter-Strike is still in the process of developing. Its appearance follows a fun and comic-like style, which comes across as harmless and entertaining. This esthetic choice was made consciously in an attempt to be especially attractive for sponsors and to clear up old problems with the image of FPSs, thereby increasing acceptance and the ease of “sponsorability.” It cannot be denied that the move marks the birth of a competing esports ecosystem. The market will let us know if there is enough space for both systems, as they are in some ways to be considered to be very similar. It is clear that Riot Games has done its homework on the key characteristics of the esports title. Aside from its beta key drop strategy, Riot Games announced that it would not immediately create a league or tournament structure similar to its League of Legends infrastructure right away but would instead give third-party organizers a chance to grow the scene and develop talent. In Q2 2020, more than 100 tournaments were organized for Valorant, second only to Counter-Strike: Global Offensive, its competitor in the FPS genre. Overall, Riot Games wants to create a platform in which they can build up business ecosystems and not be restricted by the image of their esports titles.

Furthermore, Project L, a fighting game set in the League of Legends universe, has been confirmed to be in development. This title will focus strongly on the area of fighting games in the esports sector and will aim to seize market share from existing competitors such as Tekken7, StreetFighter and Super Smash Bros. Ultimate. The esports fighting genre has a particularly strong presence in the Asian market and is expected to be established in other markets in the future. Furthermore, with League of Legends, Riot Games has one of the largest esports games in its portfolio and would like to transfer the popular lore behind it to other areas in order to enter new markets. From a brand experience perspective, Riot Games is leveraging the positive experience of League of Legends to occupy a genre that has much more potential globally than is currently used in the esports industry. It would not be the first time that Riot Games has acted as a disruptor and set new standards, filling a void that other publishers have not been able to fill. In this context, other brands may have the opportunity to invest in this segment and reach the audience. In addition, the fighting genre—and others—can be made more accessible to the existing fans of Riot Games. Overall, Riot Games aims to dominate the esports market and, as a result, to serve the various esports genres from a single source. In this way, business partners and viewers can be reached to the full extent. Therefore, the strategy is one of network building in which Riot Games wants to develop as many individual ecosystems in esports as possible and ultimately set the tone for the overall market. Moreover, Riot Games is getting serious about mobile esports. It had been rumored for several months that a mobile version of League of Legends would be launched by Tencent, Riot Games’ parent company and the world’s biggest mobile games maker. Riot Games has confirmed the name of the mobile version to be Wild Rift, with a launch scheduled to happen very soon. Wild Rift is not a direct port of League of Legends, but a version of the title that has been adapted for the mobile platform. Multiple mobile releases illustrate that Riot Games, probably under the influence of its parent Tencent, is now very serious about smartphones for reaching audiences, especially in emerging and mobile-first markets. Due to the success of League of Legends, Riot Games has many years of expertise in the esports sector and is therefore pursuing a promising monetization and development strategy for future games. Riot Games is therefore gradually closing the gap to the demand and needs of the market itself and can build on a diversified portfolio of esports titles in the long term, and is currently a successful esports publisher in the sector. But what makes Riot Games strong is not reinventing the wheel, but rather aligning the services around the esports experience, accessibility and community development with consumer needs. As a result, we may expect more improvements and innovations within the esports titles regarding quality-of-life services for content creation, sharing and socializing, as well as more tools to improve the overall esports experience along with training and analytics possibilities.

Valve—the old guard

Valve is behind two of the most successful esport titles, with Counter-Strike: Global Offensive and Dota 2. Yet esports seems not to be the top priority for Valve in the sales mix. The publisher earns money mainly through its internet sales platform Steam, a marketplace for computer games, software, films, series and computer equipment. Steam is also widely used by other publishers for the distribution of their games. The publishers act from laissez-faire to highly controlled depending on their perception of the competition in the market. So far, Valve has relied on a fairly laissez-faire approach to managing its esports ecosystem, as league operators have taken over most of the business risk involved in promoting, organizing and executing competitions, tournaments and events. This was possible because there was no real competition for Counter-Strike: Global Offensive in the field of tactical FPSs for a long time. The structures and the ecosystem have been growing here for years, and Counter-Strike: Global Offensive has established itself sustainably as one of the most relevant esports titles. The second big title, Dota2, operates with League of Legends from Riot Games in a duopoly in the multiplayer online battle arena (MOBA) genre, and the player base seems to be big and enthusiastic enough to accept both ecosystems. But here too it appears that League of Legends has gained an advantage over Dota2 over the years and the active user sales are not balanced. It is possible that this may change in the future depending on the active user and player base. The current rise of Riot Games’ tactical team-based FPS Valorant could change the publisher’s strategies. For both games, however, it can be assumed that they will continue to grow and make a sustainable contribution to the overall growth of the global esports industry, and will bring new innovations when it comes to esports performance measurements and possibilities to grow the community. These ecosystems will have a stable foundation and can further drive the competition should there be a consolidation phase.

Activision Blizzard—a changing titan

Activision Blizzard is one of the biggest companies in the larger gaming cosmos, having left its mark on esports in the past and continuing to drive the industry to this day. On closer inspection, however, some have said that Activision Blizzard is losing sight of a core factor: listening to the community and player base, reflecting and considering their needs and desires in relation to the esports ecosystem and delivering best possible experience to their audience. While Call of Duty: Modern Warfare has proven to be a hit, it is yet not a leading esports title in all global markets. So far, it has only created buzz in the US. As a result, Activision Blizzard continues to change its position in the esports segment, as the company does not always pursue strategies adapted to the user and player base and, most importantly, does not generate as many in-demand titles or innovations in its portfolio. The previous Activision Blizzard esports title Overwatch continues to experience a drop in demand with the rise of Riot Games’ Valorant. To date, Activision Blizzard’s Overwatch has not been able to meet its expectations of fully penetrating the masses as a true esports alternative in the FPS genre. This might be due to the over-regulation of competitive structures in the Overwatch League, Overwatch Contenders and Call of Duty League, as well as the licensing policies and opportunities for third-party or league operators of alternative competitions, leagues and events. Activision Blizzard has an open field in the opportunities for teams below the top products (such as Overwatch Contenders), whose scope for engagement with the community through sponsors is limited. In addition, the financial possibilities of these teams are severely deficient, as the core objective is to protect the top franchises of the top leagues. Without a broad mass of casual gamers who are enthusiastic about the game and the opportunity to participate—and who are eager to imitate their idols and enjoy the game in their spare time—a franchise league has a challenging task to make use of its full potential, no matter how professional. The development of such structures takes time and must be maintained and expanded. Slow growth, with the right sponsors and investors willing to make the journey, might be more promising compared to a top-down structure. Although Activision Blizzard has managed to place the Overwatch League a bit more in the Asian and European markets, the ambitions were certainly stronger here as well. Currently, there seems to be no indication that this strategy will change, which means that the future positive development and attractiveness of the game will be questionable in the short to medium term, with progress to be expected mainly in the US. Activision Blizzard therefore wants to remain loyal to its closed franchise leagues as a top product in the long term, and might boost the structured development of the semi-professional and amateur sector at a later stage. Even though franchise revenue has increased significantly from one season to the next, the question of additional growth impulses remains open and how Activision Blizzard will deal with the topic of sustainability and overheating. For team owners, it is therefore a long-term investment and a bet on the future. Although this approach is aimed at a long-term plan from Activision Blizzard perspective, it remains to be seen how long the enthusiasm of the viewership can last in view of the existing substitutes, such as Counter-Strike: Global Offensive and Valorant.

Electronic Arts—the giant unleashed

Even though Electronic Arts (EA) is one of the biggest game publishers and developers in the world, the FIFA series is only now starting to gain momentum in Europe. Interest saw a particularly sharp rise in 2019 that has continued in 2020. EA is trying to improve its way in dealing with the community and has started working together with the soccer association itself. Here, the plan is to transform the esports title more into a professional ecosystem, which will probably be very similar to the structures of soccer. Even if this does not seem particularly innovative it will finally provide a clear structure around which a sustainable economic system can develop. FIFA today does not yet provide a sufficient foundation for esports teams or even soccer clubs to build a positive business through its player base, reach and viewership. A much larger international audience and community is needed here, as national coverage in particular does not currently justify the effort. Although the mega-events work, as with all esports titles, the development of structures in the semi-professional and amateur sector in particular must and will be stepped up in the future. At the same time, success will depend on how EA manages to establish a stronger link to traditional soccer in order to attract more attention for future development phases and to better exploit the attractiveness of this ecosystem. The advantage for EA could be that no other esports title can rely as much on an existing physical network and image as FIFA. The trend toward an end-to-end digital and physical experience offers a lot of room for a creative design of the economic ecosystem with much added value for the community. For this to happen, however, EA has to become an even greater driver and mediator between the worlds of esports and traditional sports. Particular challenges here are that even more stakeholders and interfaces have to be served and that the sustainable integration of soccer's self-image is a special task.

Epic Games—where esports and entertainment meet—”esportainment”

The debate about Epic Games and Fortnite, and whether Fortnite is really an esport, is set to continue. The commonly used term “esportainment” describes the character of Fortnite much better and shows the direction in which direction Epic Games is moving. More than any other game, Fortnite has shown how strong social networks within a game can be while demonstrating the possible tie-ins between gaming, music and film. Unforgotten are the Travis Scott and Batman moments, which show that Epic Games is clearly focusing on the social and entertainment aspect of esports, binding masses of young players to its ecosystem and making it more attractive for potential partners to become part of it. As a result, we will see the further development of Fortnite toward an entertainment and social network. This trend will build even stronger bridges between digital and physical events once the special circumstances around COVID-19 subside. At the same time, it is very likely that Epic Games will come out with even more service innovations that will allow players to satisfy even more needs from within the game. In particular, ecommerce and integration with other social media networks like 9gag, Reddit and Instagram are possible, as are partnerships with providers like Spotify and Netflix, or even holiday tour operators. The focus is expected to be on product development, market penetration and market development, as well as a much stronger in-game integration of products and services from business partners. Epic Games can and will capitalize on its momentum and its platform as a social network, and we will continue to see big news, disruption, innovations and benchmarks when it comes to esportainment in the future.

Ubisoft—here to stay

Ubisoft has attracted a lot of attention—especially recently, with Rainbow Six Siege victories—and has taken big steps toward becoming a serious esports player. It remains to be seen how Rainbow Six Siege can further establish itself as an alternative and how the competitive structures for all types of players continue to develop. At the moment, it seems that the efforts around the expansion of these structures are getting stronger and stronger and are being pushed further and further. The starting position, with the immense number of active players and the broad gaming community around this title, could hardly be better. Ubisoft can and will certainly continue to use this momentum more strongly. However, due to its realism, Ubisoft will also have to deal with old familiar challenges regarding the tactical first-person shooter (FPS) image and sponsor needs. As a result, the title may only be interesting for markets, brands and sponsors whose ideas and image fit the character of the game. It is clear that Ubisoft is strongly focused on market penetration and market development and can already build on recent successes.

In-game advertising—a hot ride

The great popularity of esports is also pushing the topic of in-game advertising. The trend toward more digital online advertising in games will also increase in 2020 following extensive investments in esports leagues and the technology to realize it. The participating esports teams and publishers want to amortize these investments by selling broadcasting rights and lucrative sponsoring contracts. Many well-known brands can be found today at tournaments where up to 400 million unique impressions are generated and spectators actively follow their favorite teams online or on TV, sometimes over several days. From Intel and American Express to Mercedes-Benz, many sponsors are already present and are trying to link their advertising campaigns with the experience in esports games. With programmatic advertising and programmatic creation, it is becoming increasingly easy for advertisers to reach gamer target groups with automated messages. The first agencies are offering innovative formats for in-game advertising, such as dynamic in-game banner advertising. Companies can book predefined advertising space in real time during the match.

The trend in 2020 is clear: publishers such as Riot Games, Valve or Activision Blizzard are investing a lot in their leagues and in the adaptation of proven organizational structures from established sports, but are also constantly trying to create something new to avoid old mistakes. They are all sending a clear message to advertisers as well. In worldwide broadcasts via live stream or at sold-out live events in stadiums, in-game advertising will reach hundreds of millions of paying viewers and fans in 2020 and will continue to grow massively in the esports segment. In any case, the race to adapt, win the favor of the community and build the strongest economic ecosystems with sponsors, partners, investors, athletes and fans, both endemic and non-endemic, is in full swing.

Contact us

Werner Ballhaus

Global Leader Entertainment & Media, Partner, PwC Germany

Tel: +49 211 981-5848

Gian Luca Vitale

Gaming & Esports Business Advisory, Senior Associate, PwC Germany

Tel: +49 175 8534-794

Contact us